INSPIRATION! Sleep Study Results & Analysis

Note: The following was published in the April 2006 Respiratory supplement "Inspiration!"

Note: The following was published in the April 2006 Respiratory supplement "Inspiration!"

Wachovia Securities completed its study of U.S. sleep centers. Ninety sleep centers participated in the survey, however, participation in individual questions varied as responses were not mandatory. The number for respondents for each question ranged between 58 and 90. Overall, results show strong secular growth for the sleep therapy market. Some of the specific findings include:

Q&A with Ron Richard, senior vice president of strategic marketing initiatives at ResMed

Snoring is nothing to laugh about and should receive proper medical care and diagnosis to determine if a person has a significant breathing problem which can lead to serious consequences such a stroke, heart attack, motor vehicle accidents and cardiovascular disease among other issues. |

Sleep Center Capacity Expansion Continues

- On average, sleep centers report 21 percent growth in beds during the past 12 months. Respondents expect the number of beds to increase 31 percent during the next 12 months. Results support Wachovia's 20 percent obstructive sleep apnea (OSA) market growth forecast through 2007, which assumes nearly 30 percent mask revenue growth and flow generator revenue growth in the mid-teens.

- Respondents reported bed growth — an average of 12.9 beds per respondent vs. 10.7 beds per respondent 12 months ago. Respondents expect greater sleep center capacity expansion this year.

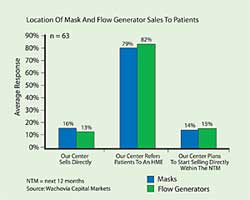

More Sleep Centers Are Selling CPAPs

- Currently, around 15 percent of sleep centers sell masks and flow generators with the remainder referring patients to a home medical equipment dealer. Around 15 percent of sleep centers plan to start selling equipment directly within the next 12 months. According to the survey, "sleep centers are more likely to provide patients high-end equipment and are less price sensitive than HMEs."

- The majority of sleep physicians and sleep center staff surveyed report sending their patients to an HME for equipment purchases. Currently, around 16 percent of sleep centers surveyed sell masks directly while around 13 percent of sleep centers sell flow generators directly. Over the next 12 months, an additional 14 percent of centers plan to start selling masks directly while an additional 15 percent plan to start selling flow generators directly over the next 12 months.

More Brand Specific Flow Generator Prescriptions

- Brand specific flow generator prescriptions account for 47 percent of prescriptions according to the survey, up from 29 percent of prescriptions in Wachovia's previous survey. Brand-specific mask prescriptions account for roughly 64 percent of total prescriptions (compared to 62 percent of prescriptions in the previous survey).

Modest Decline in Respiratory Share of Prescriptions Expected

- Wachovia's results suggest that Respironics will lose about 2 percent of its flow generator prescriptions share (currently 51 percent) to smaller firms Fisher and Paykel and Puritan Bennett over the next 12 months while ResMed should maintain its flow generator prescription share (31 percent).

- Similarly in masks, data suggests slight prescription losses for Respironics (currently 37 percent), while ResMed is expected to maintain its 37 percent share. In its analysis, Wachovia Securities states that "prescriptions are only part of the picture, however, since HMEs select equipment for patients without brand-specific prescriptions."

Q&A with Ron Richard, senior vice president of strategic marketing initiatives at ResMed

HHP: Do you think increased awareness of the sleep apnea market in the mainstream press has led to increased diagnosis?

Ron Richard: Yes, we have seen positive results based on feedback and increased activity in the sleep centers due to the efforts of joint public relations campaigns. The AASM, ASAA and NSF have all been very active in their communication with various outlets of the media. ResMed and Respironics have jointly funded and established an educational awareness site, www.sleepapneainfo.com, along with working closely with several media outlets and physicians to increase the level of awareness at the level of the general public. Just last week, sleep apnea was in a topic covered on the "Today Show" hosted by Matt Lauer. So sleep is a hot area right now and people are getting the message — snoring is nothing to laugh about and should receive proper medical care and diagnosis to determine if a person has a significant breathing problem which can lead to serious consequences such a stroke, heart attack, motor vehicle accidents and cardiovascular disease among other issues. Early detection and treatment is key to reducing health care costs associated with chronic diseases such as sleep apnea. The economics of treated vs. untreated sleep apnea is staggering. Untreated patients cost the health care system billions of dollars each year, and the treatment is simple and they can get to feeling better very quickly after treatment is initiated.

HHP: How has ResMed's marketing efforts toward sleep physicians and sleep centers facilitated this awareness?

Ron Richard: ResMed over the past four years has spent a great deal of time educating primary care, cardiology, internal medicine and other medical specialists regarding the link between sleep disorders and other comorbidities. Specifically in the areas of cardiovascular disease and recently Type II diabetes, the prevalence and links to sleep apnea is overwhelming. This is really becoming a game of "connect the dots" for the patients and physicians. Oftentimes the patient may present with the chief complaint of being tired and the physicians are looking beyond that to other issues such as sleep, exercise and diet. These elements provide the doctor with a better overall view of patients' activity both asleep and awake. For years, many people have recognized the importance of diet and exercise, but finally they are waking up the fact that they need a good night's sleep. Our marketing efforts have increased the awareness of the problems associated with sleep and other comorbidities and helped to establish the links with these diseases in cooperation with professional medical groups and partnerships. Ignorance is our biggest competitor in the sleep market, so this is an industrywide issue and needs to be attacked from many angles.

HHP: Is it true that as many as 90 percent of people who have sleep apnea are currently undiagnosed?

Ron Richard: Based on recent studies published in peer reviewed journals, this appears to be the case. And at the rate we are doing sleep studies and setting people up on treatment, it would take 20 years to test and treat just the people with moderate to severe sleep disordered breathing (SDB) at the current rates. Prevalence just in adults is thought to run as high as 20 million people and SDB does affect adolescents as well. SDB in children is thought to be as high as 3 to 4 percent, so this would be additive to the overall SDB number creating a problem of epidemic proportions. Obesity is considered a major contributor to SDB, and as noted by multiple medical journals and TV programs, we are in a crisis mode dealing with obese or morbidly obese patients in this country. Prevalence of SDB in patients with a BMI over 30 is 80 percent or more.

HHP: How has flow generator technology changed the CPAP market? Has it improved compliance rates?

Ron Richard: Huge improvements have been made in the area of flow generators. They have become much smaller, lightweight and quieter and many features that once were only available on premium devices now are commonly found on standard versions of the products. By shrinking the overall size of the flow generator, it has also helped in improving compliance since the patient can now more easily travel with their unit. The ability to manage patient data more efficiently has also improved patient care and in particular the ability to troubleshoot excessive leaks, pressure-related problems, and correct compliance issues more quickly. But the biggest improvements in compliance have come from better fitting and more comfortable masks as well as heated humidification. Masks now offer more sizes in not only nasal type interfaces but also in full face and nasal pillows. Overall we have seen reports of compliance improving over the past two to three years due to the advances made in both the flow generators and masks and should continue to see this make further strides in this area.

HHP: How can HMEs continue to stay competitive in this market when many sleep centers are selling products directly to clients?

Ron Richard: At a recent sleep meeting hosted by the AASM their projections of sleep centers getting into the DME side of the business was accelerating and would mean that almost 50 percent of the sleep centers would be offering DME at some level to patients within the next three to four years. This will change the landscape of the market and have an impact on HMEs working with sleep centers as key referral sources for CPAP patients. Many sleep centers offering DME limit this to only their private pay patients. Depending on the state they practice in and the laws related to self-referral, many labs are approaching entering the DME side of the business with caution and covering their bases before making any business plans. Also, in some areas of the country, the sleep centers are finding it difficult to get provider numbers to work with patients in certain insurance plans. Some payers feel there are enough providers in a market and are reluctant to give out additional provider numbers thus limiting access to DME. The best ways for an HME to stay competitive are the following:

- Consider opening up their own sleep centers.

- Offer better patient follow-up programs with metrics to show improvements and outcomes.

- Work closely with the sleep centers so as to understand what is driving them to get into DME.

The best thing to do is keep the communication open because in this business everything changes with time, and don't burn any bridges as the sleep center may decide that they may not want to continue doing DME after a period of time and want to work with those HMEs that stayed in touch with them. Certainly there are a number of changes in store for 2007 and looking ahead. Business owners that evolve and adapt to change are the ones who will survive and thrive in light of the pricing pressures and cutbacks.

HHP: If the AMA recognizes sleep as a physician specialty next year as anticipated, how do you think this will impact the sleep apnea market?

Ron Richard: There will most likely be more Internist becoming boarded in sleep as it is a recognized specialty. This will open up access and should improve through put of patients as more labs open and more physicians with the internal medicine group take an interest in making sleep their profession.

HHP: What do you hope to accomplish with the results of the survey?

Ron Richard: Wachovia has done this survey for a few years and this data along with reports from Frost and Sullivan and others confirm market trends. We oftentimes triangulate data points to test the robustness of the predictions and statistics in the reports. We use this information to target the environment in terms of sales, marketing and product development. The reports enable us to test our internal theories so we are seeming to be "drinking our own bath water." So in a sense they can either confirm or sometimes confuse our thinking of the trends but thus far we have been pretty fortunate to read the tea leaves correctly and respond to the needs of the market.

HHP: Describe your typical sleep apnea patient and if this has changed in the past five years.

Ron Richard: The obese or overweight patient unfortunately is still the paradigm for sleep apnea. However, as awareness increases, we are seeing that profile being altered somewhat. There are more women being diagnosed and certainly more children now being recognized with sleep apnea than there were five years ago. With improvements in technology, we are also seeing a rise in more complex patients suffering from mixed apneas such as Cheyne Stokes or central apnea requiring a different approach to treatment and even protocols for diagnosis. As more patients are being referred from cardiologist and specialists dealing with comorbidities associated with sleep disorders, this is having a dramatic impact on the patients showing up for sleep studies. In a few years, garden variety simple obstructive apnea may be diagnosed with portable home devices and patients placed on APAP systems for a few weeks to determine their pressure settings. But this first has to be accepted as a model of care whereby payers are willing to cover the patients' DME if their portable study results test positive and those results are interpreted by a sleep trained professional to ensure proper care is provided the patient.

HHP: Do you find that patients are going to sleep labs on their own accord or still following the trend of spouse/partner insistence?

Ron Richard: A predominant number of patients come into sleep labs as self-referred. In fact a recent survey showed that more than 70 percent of patients who went for a sleep study were self-referred based on discussions with their spouse, a friend or coworker and searching the Internet which lead them to talk to their doctor about their problems. The study went into more detail in this area and found on average it takes a patient almost seven years from the time they first became symptomatic before they get diagnosed and treated for sleep apnea. Obviously there is room for improvement with primary care physicians and the public to reduce this particular aspect of awareness to treatment. If we can see the same impact early detection and treatment has had on asthma in the sleep apnea sector, we will see a rapid drop in morbidity related sleep deaths that could have easily been avoided. But it took several years for the health care system to adopt simple pulmonary screeners — peak flow meters and innovations in education as well as treatment — before we saw a drop in deaths and accidents due to acute asthma attacks. Hopefully, it won't take that long for our society to realize that sleep apnea is related to thousands of accidents and deaths associated with four out of the top five causes of death in this country.

This article originally appeared in the April 2006 issue of HME Business.